How to earn more than five per cent in an IFISA

INVESTORS can earn more than five per cent by investing in the top-rated Innovative Finance ISAs (IFISAs), research claims.

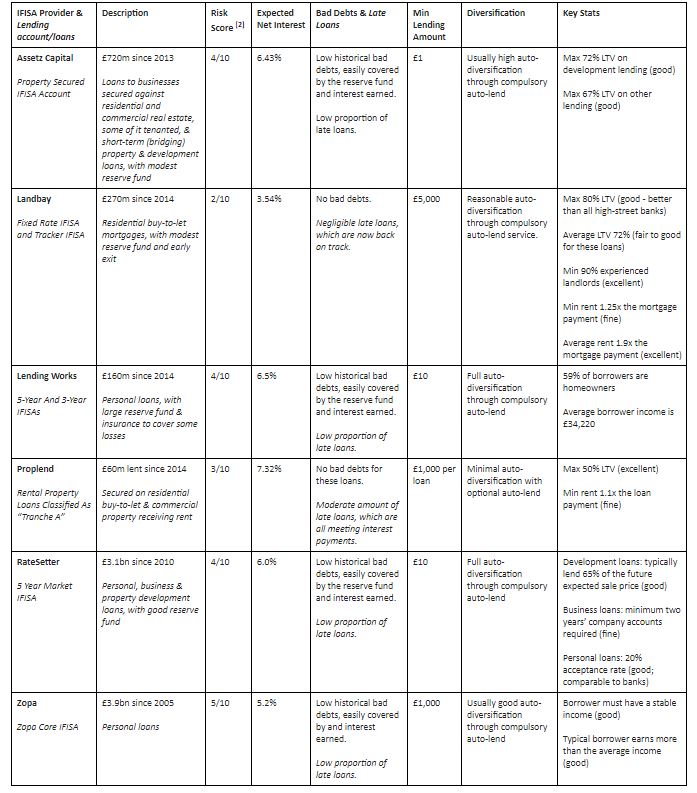

By spreading funds across platforms that 4th Way has given its highest PLUS rating, investors could earn 5.82 per cent returns, the peer-to-peer lending analysis firm said.

New IFISA funds can only be placed on one single P2P platform during a tax year, but Neil Faulkner, managing director of 4th Way, said investors could also access the returns by transferring old ISA money into the wrapper across several platforms.

Read more: The IFISAs you can open for £100 or less

The analysis assumes investors spread their money across six to 12 different P2P platforms until the loans are fully repaid.

The PLUS Ratings are based on interest rates and a forecast of the risk of borrowers not repaying their entire debts.

Its analysis shows investors could access returns ranging from 3.54 per cent with Landbay to 7.32 per cent with Proplend.

Read more: P2P lenders bullish about 2019 IFISA boost

Read more: Orca launches multi-platform IFISA

“IFISAs and P2P lending accounts, their non-tax free equivalent, have provided exceptionally steady returns that beat inflation and cash ISAs by a large margin. Investors can easily spread their money widely to reduce the risk of bad luck,” Faulkner said.

“Since investors usually lend their money from the start of a loan right until the point it is repaid, there are no massive swings in performance.

“This is a contrast to the stock market, where investor fear and greed moves prices a great deal. IFISA investors invest at a fixed interest rate that is usually set by experts and paid out to investors on a regular basis.

“Most investors are putting their money with platforms that are highly competent and have bank-level standards.

“RateSetter, for example, accepts a similar or perhaps slightly better number of borrowers for its personal loans as the high-street banks, while requiring that all business loans are secured – often on physical assets such as vehicles – and its record on development lending has been exceptional so far.”

Source: 4th Way