Making capital work

MarketInvoice’s co-founder and chief executive Anil Stocker tells Peer-to-Peer Finance News how the platform plans to double its lending this year and team up with banks while beating them at their own game…

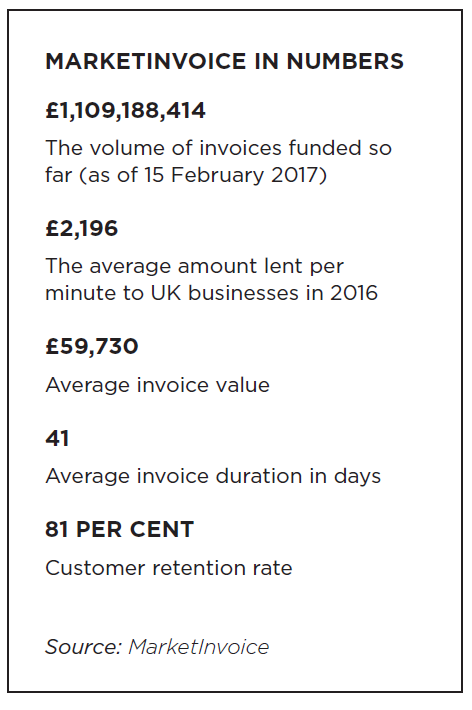

2016 was a good year for MarketInvoice. The peer-to-peer invoice finance platform quadrupled its lending over the last 12 months, bringing its cumulative total to more than £1.1bn – equating to an impressive average of £2,196 lent every minute to UK businesses.

The firm shrugged off Brexit to raise £7.2m from Polish private equity firm MCI Capital in July, made a number of senior hires and moved into a shiny new office in fintech-friendly Shoreditch.

The money raised from MCI Capital last year was primarily used to build new products, invest in automation and improve technology. The platform has spent money building up its algorithms and putting more data into its risk modelling, so that it can offer more automated services and boost its decision-making processes.

But the company has even more ambitious plans for 2017. MarketInvoice is aiming to almost double its lending to £2bn this year, aided by its new product, MarketInvoice Pro, which launched last month. It offers businesses an open funding line against their outstanding invoices, in contrast to the lender’s core invoice-by-invoice finance product.

“This is the first new product since we launched in 2012, so we’re very excited about that,” chief executive and co-founder Anil Stocker tells Peer-to-Peer Finance News.

“Pro will play a very big role in [meeting our £2bn target] because when a company starts to use Pro, they do regular draw-downs and it’s for larger amounts, so the volume that they put onto the platform is far greater than the clients who are doing invoice by invoice.”

MarketInvoice Pro is designed for slightly larger companies, who turn over more than £1m per year, compared to the platform’s original product that can be used by companies that are turning over as little as £100,000 per year.

“This is a £21bn market in the UK that’s traditionally been dominated by the banks,” says Stocker. “A lot of people will be very attracted to our new product and we’ll be able to take a big market share away from the banks.”

There are also plans for another product to be launched in the middle of this year. Stocker would not disclose any details, except to say that it was still in the invoice finance space.

On one hand, Stocker is hoping to take market share away from the banks with MarketInvoice Pro, but developing partnerships with them is also a key focus this year. This is a path already explored by several P2P lenders, such as Funding Circle and Santander, or Zopa and Metro Bank.

“You will have seen some of our historical partnerships with accountancy firms and local councils, but actually we believe that collaborating with banks is going to be an important part of the future for P2P platforms,” says Stocker.

“A lot of banks have woken up to the opportunity of partnering with fintech companies. They realise it would take them too long to build the same system that we have and there are interesting ways that we could work together. So we’re having some really great, interesting conversations there.”

Read more: MarketInvoice and Funding Circle represent P2P on fintech delivery panel

Stocker is tight-lipped about the exact details of the potential partnership, which is likely to be announced this month, but he does say that it has “never been done before here in the UK”.

“Metro Bank and Zopa was a funding partnership, but we’re also in discussions for a deeper kind of integration, where a bank would potentially refer their customers on to our platform and we would collaborate in servicing them,” he adds.

On a wider level, Stocker is feeling confident about the economic climate for his business.

“Personally I don’t think interest rates are going to go up any time soon,” he says. “But even if they did, firstly they’d have to rise a long way because they’re so low at the moment and also, if you look at invoice finance through the cycle, even in high interest rate environments, it’s still a very popular product.

“Of course, I think retail investors tend to keep more money in the bank when interest rates go up. If you’re getting two or three per cent in the bank, do you want to go through the effort of investing in P2P to get four or five?

“However, institutional investors are still very keen to make good returns in those conditions, so I don’t think that it’s really going to change the flow of capital into P2P if interest rates go up.”

With the government on the brink of triggering Article 50, many analysts and media commentators have expressed concerns about the impact of Brexit on the economy, businesses and international investor perception. But Stocker remains unfazed.

“I can’t predict the future, but what I can tell you from a ball-park perspective is that Brexit has not had a big impact on our business borrowers,” he says.

“In fact, some of the exporters have done better than normal, because they’ve been taking advantage of the weaker pound to sell into the States and other places.

“Obviously there are some industries where a recession could mean less orders coming through for suppliers, such as construction or retail, so we’re keeping an eye on that, but for the moment it’s business as usual.

“On the investor side, we have a lot of UK-based investors who are looking to invest in pound assets as much as they were before. We have some international investors who actually put more money in because the pound went down, so they were able to transfer money and deploy more. But I wouldn’t say it has impacted the business greatly so far.”

Even if there were a full-blown recession, Stocker argues that there would be a resilient demand for invoice finance. “Companies still need the cash to pay suppliers and there’s less options out there in a recession,” he says. “It doesn’t really change much about our business, but obviously we would like to be in a growing environment because it’s generally better for the UK.”

Stocker says that the short duration of MarketInvoice’s products is an added advantage. With invoices typically paid within a couple of months, the company is able to scale in and out of sectors much faster than a long-term platform.

Read more: SMEs missing out on business opportunities due to lack of finance

Looking further ahead, geographical expansion is on the cards. Interestingly, it is fragmented Europe, rather than P2P powerhouse America, that is top of Stocker’s wish list.

“First the European brand, then the worldwide brand,” he declares. “All businesses around the world have the same problem: they need cash.

“In the next three to five years, we’ll look at certain European markets. Spain is interesting, Germany’s interesting, France and Poland are interesting. Then, if we start to get into trade finance, helping people trade around the world, that automatically turns us into a global business.”

There is less opportunity to disrupt the US market as there are so many banks and unsecured lending providers, according to Stocker.

And what about a long-awaited UK P2P initial public offering?

“My philosophy is you build a great business and the exit takes care of itself,” he says. “As we get bigger and bigger and build out our tech, we become a very attractive acquisition target for financial institutions, but we can also definitely think about listing in the future.

“Ultimately it would be exciting to list a company or just keep on growing as a private company.”